If the embedded audio narration isn’t working properly or doesn’t sound good, tap this button to switch over to the podcast version.

In last month’s issue, I looked at the hidden risks in the global investment environment and how crypto isn’t too different. In this month’s issue, I reflect on the collapse of the crypto market and what comes next.

At the end of 2021, I gave prediction articles to two magazines about what I thought would happen in 2022. You can read the articles if you’d like:

In a nutshell, I predicted something like what we’re going through right now—a terrible time for crypto but a great investment opportunity for us.

I didn’t have a lot of conviction behind those predictions. They were just reflections on 2021 and some guesses about what might happen in 2022. As with all predictions, take them with a grain of salt. The market determines its own fate. It doesn’t care what I think.

We all knew the deal with crypto: hacks, scams, protocol failures, rug pulls, etc. Pretty standard stuff. The cost of doing business. Pitfalls we try our best to avoid, knowing we’ll sometimes get zapped.

Few of us knew about what was happening behind the scenes: one of the biggest trading firms lied, stole, and lost other people’s money on degenerate speculation. In doing so, they wrecked some widely-used lending platforms and destroyed trust in crypto for years, even among the most ardent supporters.

I just thought we’d have a bad year and possibly a crypto winter. Some people would go to jail. Some projects would fail. Scammers would get bored or go broke. We’d get some new laws and regulations, as well as a chance to get into great projects for cheap.

I just didn’t anticipate it would get this bad.

Yet, here we are. It will take a long time to untangle this mess—probably longer than I would’ve thought at the end of last year.

Not as bad as it could’ve been

At least this cycle was the story of cheap money chasing yield. Crypto bros and scams. Bad actors abusing the trust of others.

We can recover from that.

A lot of people cashed out—some at a loss, some at a gain. Many lost more than they could afford and many made more than they could have expected.

Aunt Sally and Uncle Morton left in October. Summer tourists left in December. Of the few businesses and pensions that took small positions in bitcoin or bitcoin funds, many pulled out in the spring of 2021, towards the end of 2021, or near the beginning of 2022. They were spared.

In the wider world, few people’s fate depends on crypto. They’re so busy getting rug-pulled by their governments and central banks that they’re hardly touched by crypto’s woes. Only we courageous few who choose to persist.

Crypto is not part of a coordinated effort to deflate the global financial system, manufacture recessions, and push small countries to the brink of default. It’s just collateral damage.

Can you imagine how much worse the world would have been if the Terra debacle and 3AC scam had unraveled after crypto had reached mass adoption?

Perhaps our fraudsters and degenerates saved the world—and our industry—from an even bigger disaster that may have come later if they had been able to stick around long enough to see the technology go mainstream and find more than a trivial place on institutional balance sheets, private portfolios, and managed funds.

No more bull, I can’t bear it

This is one reason I’m rethinking the notion of bull and bear markets.

For example, now that the dust has settled, we have a lot of evidence that our market peak did indeed come in April 2021, despite not triggering extreme levels on many technical and on-chain indicators.

In fact, technical and on-chain indicators suggest the peak came in January 2021—meaning the market spent most of 2021-2022 at higher prices than it did at its technical and on-chain peak. Should that happen?

The “bear” market of 2021 lasted only two months and the overall market dynamics matched typical consolidations within an uptrend. The peak came months later. Some altcoins and NFTs went higher in November than during altseason. Should that happen?

We get 100-300% upswings during bear markets and 40-50% crashes during bull markets. Should that happen?

Maybe we need a new mental framework for crypto. Instead of bull and bear markets, how about “Bubble” and “Non-Bubble” markets? Grifting season and building season?

Perhaps there are only two modes for this market: quiet development and FOMO MANIA.

They dance on our graves for three years, we dance on their graves for a year. We spend three years building a better world, then spend one year making fools of ourselves. Once the party ends, some people stick around. Rinse and repeat.

Let’s think about it that way, instead of bull and bear markets.

At least then people will recognize what kind of crypto experience they’ll get: a chance to make fast money or a chance to contribute to the building of new financial systems.

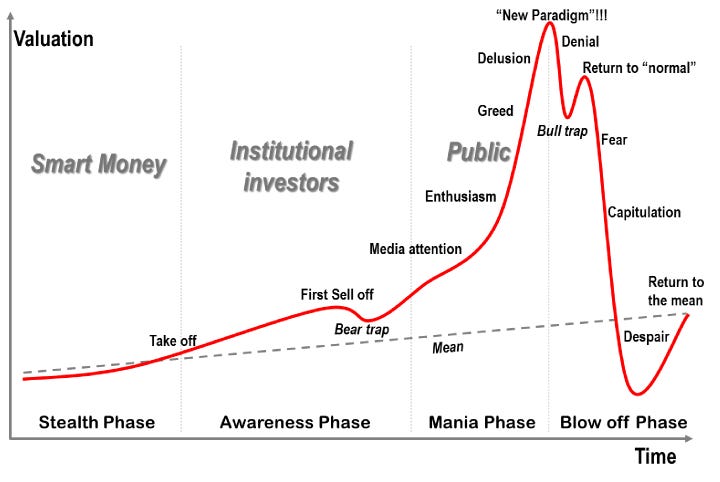

Perpetual bubble machine

In the coming weeks and months, prepare to see a lot of “Anatomy of a Bubble” charts. Here’s one:

I used to have this chart on my website to “track” the bubble, which I put on a timeline from 2012 to 2026.

For some reason, I stopped tracking it and I can’t remember why. Maybe because I thought that it may have led to 100trillionUSD blocking me? On the same page, I posted a separate “mock-to-flow” chart and said it was “like the stock to flow but with more bullshit.”

(BTW S2F is as valid now as it’s ever been.)

In hindsight, I should’ve kept the page and added my U2R model, which is also based on a line on a chart that somebody made up.

Looking at the chart each day or week would’ve served as a visual reminder that this market is one bubble cycle after another, constantly, on small timeframes and big timeframes, always masked by extremes in price and volatility, always with different contours and conditions, always with the same result.

Crypto markets move in rhythm with humanity—a perpetual bubble machine, repeated over and over on the shortest timeframes and longest time frames, in two-day cycles, altseasons, two-year cycles, four-year cycles, and ten-year cycles.

Like this:

Each bubble can last far longer and go way higher than you think possible or far shorter and way lower than you could ever expect.

The hard thing about having so many bubbles over such varying timeframes and price ranges?

You never know where you are in the cycle.

Priya in the park will always tell you the market will crash, it’s just a matter of time.

Eventually, she’ll be right. How many opportunities will you lose while you wait for that?

Tony on the TV will always tell you the market will go up, it’s just a matter of time.

Eventually, he’ll be right. How many opportunities will you lose while you wait for that?

Everything seems inevitable in hindsight. It’s never that way in real-time. What happened this year could’ve happened last year, the year before that, two years from now, or four years from now.

Timing is everything

Michael Burry got famous for betting against the US housing market in the mid-2000s. He made a fortune for himself and his clients.

Supposedly, he was months away from running out of money to fund his position. If the housing market had taken an extra six months to burst—or deflated on its own—he’d have lost his bet bigly.

Also, his warnings came several years before the peak, when you could still buy a house for a normal price with a reasonable down payment and terms that made sense for your income, goals, and lifestyle.

In other words, if you’d have limited your exposure to the housing market and its excesses, you would’ve done ok whether or not Michael Burry was right or wrong. You wouldn’t have had to time the market.

If he was right, you’d take a hit on paper but get through it. Depending on how you structured your finances, you may have even had a great chance to acquire more real estate at a discount in 2008, 2009, and 2010.

If he was wrong, your house would keep going up in value. You’d win either way.

With crypto, we’ve dealt with the same problems time after time. Tether, rehypothecation, Ponzi schemes, vaporware, unfulfilled roadmaps, scammers, undisclosed shills, regulatory threats, bans, the list goes on.

Why do people assume these problems couldn’t have gone on for a few more years? What makes people so certain that these problems would ever come to light? That those risks would ever come true? Why did they have to come out now, not in two or three years from now?

In the traditional financial system, people have done bad things forever. We’ll find out exactly how bad those things are this year, as tighter monetary policies and bankruptcies reveal shenanigans every bit as reckless as what you find in crypto.

In every walk of life, you get rumors, lies, cover-ups, and Cassandras whose prophesies never come true. Chicken Little was wrong. Risks pop up, then disappear or work themselves out. People adapt and adjust to the changing circumstances. Humanity’s creativity and resilience change our common destiny.

You plan and prepare for something you believe is certain, but never happens. I did this with the metrics I use for the “peak” signals. I set my triggers too high. They never triggered.

While it’s easy to worry about UST, Celsius, 3AC, and the liquidations yet to come, remember: with crypto, bubbles grow and burst all the time, in big and small ways, over long and short timeframes.

If you sold the peak of every little bubble—“local tops,” as the traders say—you still might end up worse off than somebody dollar-cost averaging the whole way. In this market, the price can go way higher for way longer than you think.

Too often, you sell at “the peak,” then watch prices go up even more. Once they fall back to you, they’re still at a higher price than what you sold at.

Then, the moment you think they’ll go back up, the market tanks.

Somebody else always knows better, but I don’t

How do I deal with this uncertainty?

Buy low and let the market do what it wants.

When prices go down, I buy more crypto cheaper. When prices go up, I set aside fresh cash for whenever the price goes down again. I spread my buys across several days or months. When the market goes up before I finish averaging in, I sit on my cash and wait for the next opportunity.

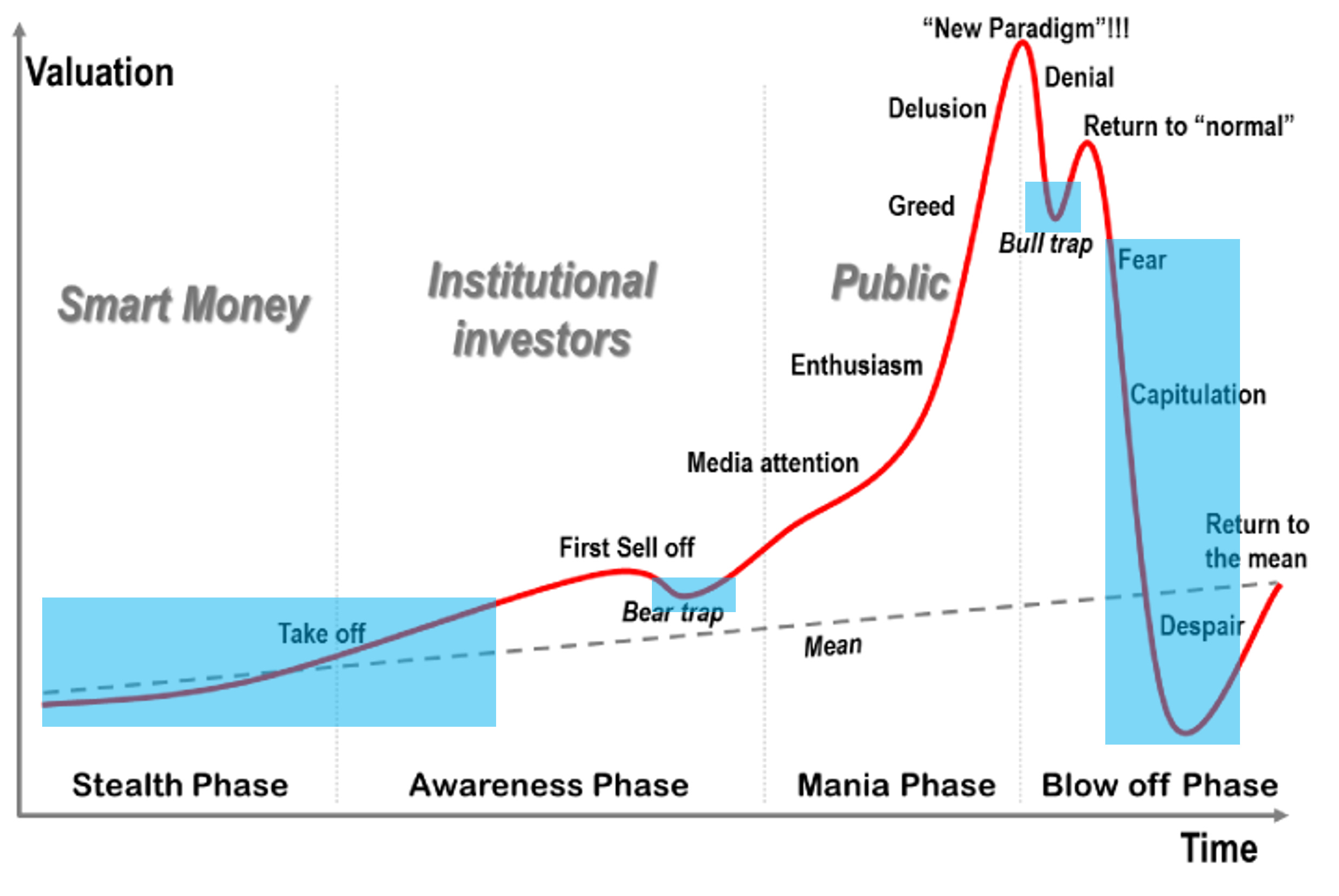

To help me manage the market, I follow my new plan.

It’s a change from the old plan. That plan bought too high. Under the new plan, you’re down as much as 45% or up as much as 400% but probably closer to down 25% or so.

(Under the old plan, you're doing worse.)

With both plans, you generally buy whenever the bubble cycles go into these blue boxes:

Yes, that means buying the downside after the end of the bubble.

Why take that risk?

Because at any given moment, it’s hard to tell whether that final drop is a bear trap, bull trap, or blow-off phase until after the pattern completes. This market does crazy things, usually when you least expect it will.

You’ll find a lot of glad-handing on Twitter from people who say they played this drop well, but half of those people bought into the market at $53k or $65k and pulled money out from stop-losses at $40k. Some of them are still down on their investment, possibly even more than you are.

Unfortunately, my old plan bought too high, too soon. Should’ve waited for the break of $40,000 in January, an area of technical confluence and a “lower low,” one of the two criteria for a bear market and confirmation that the larger uptrend had ended.

If I’d switched to the current plan sooner, we would’ve had an extra six weeks to set aside money. We also would have bought at a 20-25% lower price. I regret this deeply and changed my plan accordingly.

What does recovery look like?

While today's crypto market continues to tumble with no end in sight, that will change.

Bitcoin will recover. The altcoins that are destined to go to zero will still go to zero (perhaps sooner than we used to think). The altcoins that are destined to succeed will still succeed (we don’t know which ones yet).

Deleveraging speeds up that process.

Next up?

Once we work through the 3AC mess and its implications, expect a lot of changes. Wall Street, non-governmental organizations, and regulators will shape the next few years.

If you have a chance, read Bitcoin or Bust: Wall Street’s Entry Into Cryptocurrency. It’s a little dated but the general ideas are still valid.

(You get Bitcoin or Bust and my other books for free with a premium subscription.)

I expect we’ll get regulations, litigation, and probably more engagement from legacy financial companies. Should make for some interesting debates about the rules crypto will have to follow.

The US government will play its role, too. By the end of 2023, it will make bitcoin a part of its financial system, and by extension, the world’s regulated markets. Congress and the administration want this to happen. All that’s left are the details, which could take some time to figure out.

That doesn’t mean bitcoin’s price has to go up. People may never buy it again. It took a decade for the world to come back around to gold. Lots of assets have a place in the US financial system, but they don’t always go up. Market forces still apply.

It just means bitcoin will have relevance for a very long time. As long as the technology continues to evolve and the network continues to grow, you will have an investment opportunity—even if FTX and Crypto.com can’t stay in business long enough to keep their branding on sports arenas.

Does that mean another four-year cycle that sends bitcoin’s price to $500,000 and gives us another FOMO MOON LAMBO altseason?

Maybe, maybe not.

What’s wrong with owning a stake in an emerging asset that has tremendous growth potential? Would you be mad if bitcoin’s price *only* went to $100,000 over the next three years?

Wouldn’t it be nice if new money came into the market without pumping everything to the moon? No more cycles and crashes? Real growth and traction?

Instead of speculative enthusiasm, we’d get plain old enthusiasm. That way, the technology will succeed when it’s ready, not when you want to cash out.

Mark, if you’re so confident, why aren’t you going all-in now? Fire sale!

Don’t be ridiculous.

I have a lot of confidence in my house but that doesn’t mean I’m going to put all of my money into it.

We live in uncertain times. There’s nothing wrong with putting limits on your investments so you can spread your risks without sacrificing your opportunities.

I also have a lot of confidence in my ability to not die. But I have term life insurance anyway, even though—if all goes well—I will lose 100% of my investment and the policy will expire worthless.

Sometimes, restraint is the better part of valor.

The point is to force yourself to take advantage of the downturns. That’s when you get the best value for your investment. Do that and you don’t need to take excessive risks or chase after the market.

What’s the next narrative?

Same as all cycles: price goes up long enough for people to think it will keep going up. Then, they will find the narrative.

Unless the global return to financial normalcy hurts people so much that they feel compelled to flee the traditional financial system, I suspect the next cycle will run on the assumption that “it’s safe now.” If Las Vegas can turn itself into a family-friendly travel experience, crypto can turn itself into a legitimate industry, too.

That all depends on whether we can fix the UST and 3AC mess without blowing out the market. Then we can turn a story of disaster into a problem that cryptocurrency can solve.

With blockchain and crypto, you always know that your money exists. You can verify it on the blockchain. It’s not a promise, handshake agreement, numbers on a spreadsheet, or attestation for the public.

What happened with 3AC? We don’t know, most of it happened off the books. On-chain analysts can find evidence of only some of their positions.

What happened on-chain? Orderly liquidations of over-collateralized positions (with some governance failures sprinkled in).

People failed. Protocols simply delivered the consequences.

Crypto can offer a safer, more transparent, less expensive, and more inclusive alternative to legacy financial systems and huge corporations. Combined with regulations and actual real-life crypto applications, this technology will seem legit (if still experimental).

On top of that, the next few years will bring cool projects like Soltype, Readl, AtomicHub, Emanate, Common Ground, and other Web3 networks that leverage NFTs and DeFi into real-world experiences. Opennode and Strike can already process payments with more privacy and less cost than traditional payment processors.

Coinbase is working on an integrated NFT/Metaverse gateway that will patch into DeFi protocols—without asking anybody to touch crypto, just their self-funded wallet linked to a bank account or filled with USDC.

Uniswap is integrating an NFT marketplace for crypto-natives.

Many great projects have ample funding, strong communities, and interesting technology. They toil in the background, out of the limelight. Over the next few years, some of them will step into the real world and remind people that crypto can do more than “go up” or crash.

This will all give crypto a sense of legitimacy it sorely lacked this go-round.

A long row to hoe

But that comes later. It will take a long time to build trust after the UST debacle and its consequences.

Crypto is probably not as dirty as other industries, but it’s far more transparent. So are many of the people who work in it.

Until we wash away the filth, they can’t shine. That is the immediate next step—cull the herd.

In the past two months, we’ve endured a constant run of forced selling from diamond hands, HODLers, and recently, miners.

The very people who normally set the floor for prices.

As a result, the floor collapsed. The question is how much more selling pressure will come from miners, further liquidations of borrowers, and people who sell the bitcoin they get from the forthcoming Mt. Gox settlement later this year.

Until we get some new buyers, it’s not really important whether the price goes down to $14,000 or up to $30,000. You have plenty of time to accumulate.

Are you worried that the market will keep going down or never recover?

Whenever you think the market might drop—whether because it’s too high or too low—think about taking a short position. You can do this with the BTC3R leveraged short position on Bitoffer.

That way, you can profit from the drops without selling your crypto.

If the market falls, you make money and keep your crypto. If the market rises, you lose money but keep your crypto.

While that may seem risky, remember that this market spends more days going down than it does going up. Also, when you sell, you basically take a short position on the market anyway. And, is it any less risky than borrowing against your crypto to buy more crypto?

Of course, if you need money, that’s a different story. But if that’s the case, you may want to think about whether you want to risk your financial welfare on the future of a speculative asset class.

Still depends on the greater fool

Yes, of course. Such is the nature of investing. You always have to rely on somebody to come along and pay more for what you don’t want anymore.

Whether that’s Microsoft stock, metal bars, a boat, a bond that you need to sell to raise cash to cover a margin call, or a house.

Yeah, but houses have real utility. Bitcoin does not.

Factually incorrect.

Bitcoin allows you to send money electronically to anybody, anywhere, anytime, in any amount, without restriction, without giving away your sensitive personal information or control of your assets, with certainty that your transaction will go through and every payment you receive is authentic and valid.

Does that mean it’s worth $20,000 per coin?

I don’t know, but that’s what it costs.

I’m pretty sure the land beneath my houses and the structures themselves are worth a lot less than what people are willing to pay for them. There’s no reason you can’t get land and structures every bit as good as mine somewhere else for a lot less.

The market disagrees. Who am I to fight it?

As a result, I get to live in or rent out a house for 20 years, build equity and pay down the mortgage, then sell it to some losers who think they’re getting a great deal but they’re really just getting an arrangement of wood, brick, and metal that they’re always going to have to fix and pay taxes on.

Fools.

Never again

Some say this market will never come back. It’s done. Crypto is dead. Everybody lost all their money. Nothing works. This time is different.

That seems reasonable, but I’m not one to bet against history.

My biggest fear?

Next time, this bubble will be worse because we won’t have Tether FUD, cringy shills, bizarre memes, crypto bros, and central bank policies to scare normal people from investing.

Fewer people will wonder what bitcoin does because we spend so much time educating them about it.

Regulations will make it seem ok to put a little money in. On-chain experts will police the markets. Lots of legitimate, professional people from legacy finance will have their compliance department’s approval to get 401(k)s, pensions, and common people to put a little money into crypto and crypto funds because “it’s safe now.”

Some projects will produce viable technology that works at scale.

And it’s that next bubble that wrecks the world—not because people put money into a risky, volatile asset that they didn’t understand, but because they put money into a risky, volatile asset that they thought was safe.

It’s on us to make this market safe. Let’s hope we succeed.

Relax and enjoy the ride.

Share this post