If the embedded audio narration isn’t working properly or doesn’t sound good, tap this button to switch over to the podcast version.

In last month’s issue, I looked at the macro investment environment and what it means for crypto. This month’s issue looks at the hidden risks in the global investment environment and how crypto isn’t too different.

Many months ago, I had a call with a consultant who warned me the world’s governments would crush crypto.

It turns out we can do that just fine on our own.

While crypto’s not the only market that suffers from excessive greed, scams, and a complete disregard for the welfare of others, it’s the only market that people like us can easily access.

On the way up, it’s great. On the way down, it’s horrifying.

Bond traders are no less ruthless and callous than crypto traders, but they deal with complicated financial products in an opaque market. In crypto, we can see everything on the blockchain, in trading charts, and through on-chain data. Much scarier.

Some bonds lose 50-100% of their value over time. Years, in some cases. So long and gradually that most people don’t even notice.

Some cryptocurrencies make the same trip in weeks or months—so fast, we can’t help but notice.

Cruel market, this.

It’s hard to care about a small South Asian country that has no fuel, money, or food, and just defaulted on its loans. Over 20 million people will suffer as a result and nobody knows what countries and funds have exposure to its bad debts.

Who’s next? Sri Lanka first, then Malaysia? Egypt? Pakistan?

It’s natural to freak out about a promising altcoin that got trapped underneath a stampede to exit *everything* in crypto. That’s your money.

Sri Lanka is somebody else’s problem.

Until it’s not.

Elephants in the room

This is not the first time I’ve talked about debt markets.

Boring, I know, but far more consequential than crypto.

Let’s not get too into the weeds. I don’t want to scare anybody too much. I’ll just touch briefly on two types of debt that the legacy financial system may have taken for granted.

Financial products built around junk bonds.

In the US, Wall Street has invested at least $850 billion in collateralized loan obligations, an alternative to junk, er, “high-yield” bonds.

What’s a CLO?

It’s a combination of debts from high-risk businesses. Investors buy the portion of the CLO that matches their risk tolerance.

While the idea seems ok, it’s basically a corporate version of the mortgage-backed securities that led to the global financial crisis of 2008.

While the CLO market is not as big as the MBS market, you never know what’s lurking in the shadows. Many of those businesses have no profits. Some used the proceeds to invest in high-risk business opportunities.

Now that the US economy shows clear signs of slowing down, when will these businesses get the revenue necessary to pay back their creditors?

Nobody’s tweeting about that, but maybe they should.

Sovereign debt.

Governments owe a lot of money and their growth can’t seem to keep pace. China has a debt-to-GDP ratio of 300% and the US is trying its best to catch up.

What about smaller countries? The kinds of countries that don’t have leverage over their creditors? The ones that can’t service those debts with elegant financial and accounting tricks?

At the beginning of this issue, I mentioned Sri Lanka. I don’t mean to pick on the country and I hope everything works out. I chose Sri Lanka because it only just defaulted. It’s timely.

Is this an isolated incident? One unfortunate country that got in over its head?

Or is this the first domino to fall in a larger debt contagion? While you fret about Tether’s reserves, did you check on any of the countries in the IMF Global Debt Database?

Mark, this is a crypto newsletter. We have enough to worry about, do you need to remind us how bad it is in the real world?

Yes.

If you think you’ll find safety in other markets, you need to know what those other markets look like. Should any of those “safe, regulated” markets fail, it will make UST’s collapse look like a $300,000 NFT rug pull.

Borrow money now?

In recent updates, I showed some crazy, coincidental, seemingly-out-of-nowhere similarities between this month’s crash to $25,500 and the 2015 crash to $153, a generational bottom.

Some people have asked me whether it’s time to “back the truck up” and borrow to buy bitcoin.

My short answer?

I’m ok with you doing that, but there’s no way I’m going to do it. Have you seen what’s going on in the world today?

My long answer: watch this video.

In fact, I revised my plan for bitcoin’s bull market.

(I know, I know, as I said in February’s issue, I’m keeping the title the way it is.)

For a long time, I was proud to say the plan makes sure we buy when the market’s not likely to go much lower for much longer. “Lower” means 50% or less, “longer” means a few months.

I can no longer say that. My plan failed to deliver on its promise. On May 12, you might have been down more than 50% and clearly “a few” months does not mean “half a year.”

Also, we never hit any of the markers for the peak but still fell lower than any non-peak stretch of time except the March 2020 crash. And we may not be done falling. It’s worth questioning whether the plan works.

After reflection, I now have an approach that hopefully fits better with the current mood of the market and my own lessons learned.

Substantively, it follows the same concept and execution, but it’s more flexible and better adapted to our present circumstances. Like the old plan, it beats dollar-cost averaging with less effort and risk.

I plan to revisit this plan once the market picks up steam. See the new plan.

Under the old plan, you’re down as much as 42% or up as much as 450% but probably closer to down 25% or so. With altcoins, you could be up or down a lot more.

I expect this new version will do better.

No escape, no surrender

One thing that hasn’t changed?

The traditional financial system has turned safe investments into guaranteed money-losers and stripped risky investments of their upside. You can’t even go into cash anymore—unless you’re talking about US dollars. And even then, market analysts wonder if USD has peaked.

What if crypto is the escape?

No, Mark, when people lose their jobs, the first thing they’ll sell is crypto!

Yes, most people, when forced to choose between food or crypto, will sell crypto and buy food.

When you assume that means the market has to go lower, you have to assume two things:

Enough people will lose their jobs to matter. Crypto’s a niche market and only a small portion of the world’s population owns any. Even in times of “high” unemployment, a lot of people have jobs. In general, people in crypto tend to be younger, wealthier, and better employed, according to numerous surveys over the years. The very people who tend to use crypto as an investment are the very people who are most insulated from economic danger. Will a larger global downturn make that much of a difference for the people who want to put money into crypto?

People have (or still have) crypto they want to sell. We know institutions and tourists left in December 2021 and January 2022. We saw this happen in real-time. Our most recent collapse wiped out fence-sitters, VCs, and people who borrowed against their bitcoin at $50,000-60,000. What if almost everybody who’s left in this market will stay regardless of global financial conditions?

Nobody can say for sure. Maybe “the world’s going to hell so bitcoin must crash to $14,000” is 2022’s version of “printer go BRRRR so bitcoin must go to $288,000.”

The question is, will people trade a high-growth asset at a low price to get some other asset that might also collapse?

Complacency kills

Some people seem convinced that we are on the verge of a global depression or, at the very least, a long bear market for equities and a major worldwide economic downturn.

US GDP and manufacturing were both negative in Q1. Anybody looking for a US recession is already halfway there. What’s it like in your country?

Some people seem convinced that everything will work out ok. Turbulent times ahead but nothing too serious.

In the US, corporate expenditures, home loan-to-value ratios, and consumer behaviors don’t match what you normally see when staring down a financial disaster.

Until they do.

While it’s nice to have TIPS, home equity, cheap lines of credit, and cash to fall back on, most people do not have any of those things. That makes it hard to ride out the crypto waves.

Still, I sense complacency.

On the one hand, many people say “200 WMA,” “supply shock,” “bottom’s in,” and “escape velocity” means the worst is over.

On the other hand, we see a descending triangle forming on the daily trading chart, government crackdowns, Celsius and Tether FUD, and failed cycle/data models. “This time is different.” “Crypto has not lived thru a recession.” Therefore, the worst is yet to come.

What happens if we get something in the middle? The crypto market goes sideways for a year, up 50% and down 50% before it resumes its natural path upward?

While I appreciate strong convictions loosely held, it’s hard to pick one side or the other. We’re sailing in uncharted waters.

Cycle says . . .

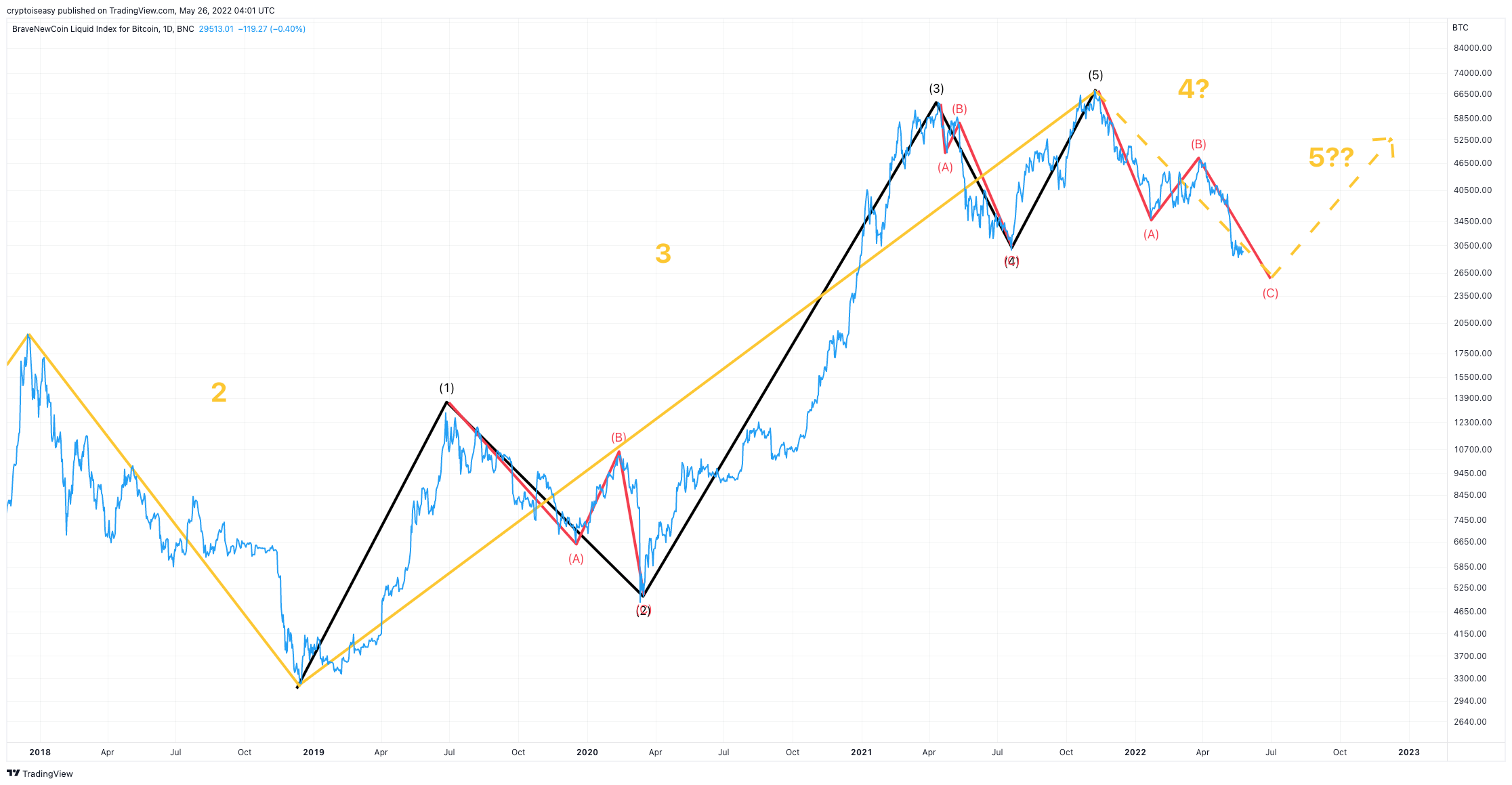

While bearish analysts insist the market will rally soon, they’re not calling the bottom. Cycle theories say the peak is in, no new all-time highs in 2025.

From a technical perspective, today’s conditions resemble December 2018 and January 2015. I covered this in several updates for paid subscribers.

If this market acts as it did in January 2015, bitcoin’s price will go up and down for the rest of the year, but not lower than $25,500.

If this market acts as it did in December 2018, bitcoin’s price will drop to $22,000 or $14,000 very soon, then hit $70,000 in January 2023. That would mean a peak in November 2021, a bottom in May or June 2022, and a new all-time high in 2023.

This begs the question: can you have a new all-time high in a bear market?

Some say we already did—in October and November 2021. April 2021 was the true peak.

Tough to say for sure. In October and November, trading indicators and on-chain data showed none of the extremes that characterize market tops, despite the higher prices.

(To that point, analysts still debate whether $69,000 is a “higher high” or “double top”).

From November to today, bitcoin’s price dropped less from top to bottom than it did in March 2020 and or any of the previous bear markets.

Unprecedented—but is it really different this time?

That aged well

Last month, somebody commented on an article I posted in February 2020, speculating that bitcoin’s price was in wave three of an Elliott Wave cycle, one way to measure market movements.

That person said “Bro , do you really know the elliott wave theory? , this article it's so wrong.”

I said “no, but it fits:”

Fortunately, I’m writing this more than two years later, so we have the benefit of hindsight. At the time, I was just drawing doodles. I posted other articles suggesting other potential outcomes, I guess they didn’t stick as well as this one did.

As with all technical analysis, you can only confirm the pattern once it’s completed, and it looks like a Wave 3 to me.

If that’s right, we’re in Wave 4, a corrective period before one final leg up. For the past six months, we have followed an a-b-c correction pattern.

The question is, at what price does that “c wave” end? Did it already complete?

It seems silly to think the bear market’s over. Probably as silly as this observation from February 2020.

Similarly, not something to act on.

In this market, sometimes the silliest ideas end up coming true and the most obvious ones never work out. Like my data model, U2R.

According to this model, bitcoin’s fair price is $75,000. Whatever that means.

(I don’t know. It’s just a model.)

Small things change, big things don’t

Are you worried that our crash to $25,500 signals more pain ahead?

For weeks leading up to April’s drop below $39,000, I told paid subscribers about the notable lack of buyers, the noticeable drop in buy-side liquidity, and the specific situational risk that a drop below the mid-$30,000 range would force liquidations of people who borrowed money against their bitcoin in October and November.

I added the following note at the end of my weekly rundown on April 24, 2022:

Consider pausing your investments…

…I’m honestly not worried about anything [at that time], in fact, we still see a lot of strength in the market.

That said, here are the conditions we’re in for the short-term:

Liquidity is basically non-existent. That works both ways—a small short squeeze sends prices way up, a minor sell-off triggers a catastrophic fall.

Leverage is still very high relative to the number of bitcoins available to buy and sell at this moment.

It’s likely a lot of people borrowed against their crypto to put money into the market. That money already went in as buying pressure. There’s probably not much more coming in behind it. As a result, the risks are skewed to the downside.

We don’t have a lot of new money coming, at least not enough to show up in any of the data I look at.

Selling comes in clumps, buying comes constantly but mostly from people already in the market. As a result, a single big whale or miner can sell us into oblivion or cause a panic with a relatively small sale—even though the overall market shows a lot of conviction…

…this is a purely situational strategy that I am applying only in these specific circumstances…since we’re already pretty well invested [after buying for most of 2022], we have the luxury of tapering or stopping our buys.

On top of that, we saw a drop in the total amount of stablecoins and persistent net outflow of stablecoins from exchanges. The safety net was getting weaker. A cascade of liquidations would cause panic among people who would have otherwise HODLed or bought more.

Did that mean the market had to crash?

No.

While we didn’t see much buying, we didn’t see much selling, either. With few bitcoins on exchanges, a trivial purchase could have blasted through the order books and sent the market zooming.

That didn’t happen.

Sometimes, bitcoin’s price goes down and crypto projects blow up. This happens in bull markets, bear markets, upswings, downswings, and pretty much every market condition. This time, it happened at a time when we didn’t have any way to cushion the blow.

No doubt, the crash scared away money that would have otherwise come into the market. It also crushed a lot of people who were already in the market. It’ll take a while for people to trust crypto again.

In a larger sense, nothing changed. Bitcoin hasn’t changed. Ethereum hasn’t changed. Your favorite altcoin hasn’t changed. The global financial situation hasn’t changed.

Time will tell whether that’s a good or bad thing. Sometimes, restraint is the better part of valor.

Either way, all of the risks and opportunities you had in 2021 remain. Except now, those risks cost less and those opportunities offer more in return.

Time is on your side

For bitcoin, any price between $22,000 and $150,000 fits within the range of normal prices. Many altcoins now trade at 2020 prices or lower.

You can get the results you expected in 2021 with half or one-tenth of the money you needed back then. The difference is, you’ll have to wait a while longer to see that investment bear fruit.

On the other hand, you don’t need to rush anymore. You can take your time, put in small amounts, and work yourself into the market slowly.

What will you do if we get that relief rally or short squeeze that so many people expect?

You can set aside fresh cash for another opportunity. You’ll win either way.

If that rally turns into a new bull market, you’re set. You’re in. You can let the value of your crypto go up. You don’t need to put more money in.

If that rally fails, you’ll have more money to bring into the market on the way down.

Know thyself

The question is, what does “win” mean to you?

Good traders will lose at least 50% of their trades. The best will lose 60% or more. If you aggregated the scorecard for your favorite influencer’s “calls,” I'd wager that they’d all be about 50/50.

How can you lose half of your trades but call yourself a winner?

Risk management.

When you win, you win big. When you lose, you lose small. Repeat that over time, and you’ll do fine.

I don’t trade, but I played baseball when I was younger.

In baseball, everybody thinks strikeouts are bad, but if you’re swinging for the fences, you’re almost certainly going to strike out more than somebody who’s just trying to get on base.

That’s ok. You only need to hit a few home runs to make up for the extra strikeouts. A home run is worth four hits, on average. Sometimes, you get singles and doubles—those are good, too.

Fans complain that’s boring. Purists think it’s bad. You spend a lot of time on the bench rather than on the base paths.

It’s not the only way to hit a baseball, but it works.

Do you want to flip cryptos for quick cash or find those 100x moonshots?

If you want to flip cryptos, then wait for altseason. Once it comes, buy random alts and sell each of them after they go up 50%. Altseasons are rare and fleeting things. We may never get one again. Get in, get a little money, and get out as fast as you can. More fun than throwing dice at the casino.

If you want to find those 100x moonshots, buy now and stake, use, HODL, and leverage your altcoins as you feel comfortable. Some will go to zero and a few will deliver 100x returns. Overall, you’ll end up 5x above whatever you thought you would’ve gotten in April or November 2021.

One way gets you a 50% return. The other way gets you a 500% return.

But you can’t do both at the same time. Which do you prefer?

Once the market turns around, you may have to come in with a lot more money if you want any chance to get the results you imagined you’d get in 2021 (i.e., 2x on bitcoin, 5x cumulative on altcoins, once you average winners and losers).

Even then, you might lose money. Same as in 2021.

In today’s environment, you have to overcome VCs dumping as their tokens unlock, project teams running out of money, community projects disbanding, inflationary tokenomics that dilute the value of your tokens, and the stress of putting money into an asset that dies.

Even then, you might lose money. Same as in 2021.

What you should do depends on what you want to get out of this market.

I prefer the slow money path. I have enough things to worry about in life, I don’t need to add crypto to the list.

My portfolio strategy diversifies among different types of assets. When one goes down, another goes up to balance out the difference. You can move wealth from one asset class to another as opportunities arise.

For the past few years, I’ve slowly increased my allocation to crypto. A gradual rotation, simply because the market’s so volatile I can’t get too risky.

You probably manage your money in a different way, with different goals. Do what feels best and works for you.

Broken record

If you’ve subscribed to me for a while, you probably get tired of hearing me say the same things again and again.

Why do I do it anyway?

Because people hear me differently when the market’s going up than when it’s going down. Also, I get new subscribers all the time. My analysis changes often but my beliefs rarely do.

If I’m going to be damned, at least I’ll be damned for who I am.

For reference, here are my beliefs:

You can always make up for bad timing. Complacency kills.

You don’t need crypto to make money. Your time, talent, energy, and innate skills are worth far more than any speculative financial asset.

Embrace uncertainty. Without it, you would not have these investment opportunities.

All financial assets come with risks, even the safe ones. Sometimes, the “safe” assets are the worst—they lull you into a false sense of security.

Crypto markets rise in a two-step process: crypto flows to people who want it more than they want their government’s money, then prices go up long enough for people to think prices will keep going up. Everything else takes care of itself.

At any time, the range of realistic outcomes is vast.

Bitcoin is the best risk-adjusted investment opportunity that people like you and me can make right now. Some altcoins will do very, very well. Most will not. Try anyway.

Nobody knows how to properly value altcoins. Each one is either massively overvalued or massively undervalued. It will take years to sort out the winners and losers, what works and what doesn’t, and what metrics matter.

Hard times make strong people. There are a lot of things to worry about in life. When it comes to crypto, a little goes a long way.

Do what you can now, stop when you need to, and make sure to take care of whatever matters most to you.

Crypto will always be here when you want it.

Relax and enjoy the ride!

Share this post